The Instant Payment Regulation

Why is it important to you?

7/9/20242 min read

As businesses, banks, PSP’s and consumers eagerly await the transformative shift towards real-time payments, the regulation stands to redefine the very fabric of Europe's economic interactions, heralding a new age of financial immediacy and security.

But what exactly is the Instant Payment Regulation?

Before delving into the IPR, I would like to look into the Wayback machine. SCT Instant was launched in 2017. Despite its mission of improving the speed, security, and cost of instant low-value payments within the Single European Payment Area, the adoption by the end of 2022 sat at 13%. Hence, the IPR can be seen as a reaction to the failures of SCT instant.

The IPR introduces rules for instant credit transfers in euros within the Single Euro Payments Area (SEPA). These rules apply to both national and cross-border transactions.

What Are Instant Credit Transfers?

An instant credit transfer is a type of payment where money is transferred immediately (in less than 10 seconds) at any time of day or night, every day of the year.

Who Must Offer Instant Credit Transfers?

Payment Service Providers (PSPs) that offer regular credit transfers must also provide instant credit transfer services to their users (both individuals and businesses).

The goal is to encourage more people to use instant payments across the European Union.

Availability and Reachability:

PSPs offering instant credit transfers must ensure that all payment accounts they manage are reachable 24/7/365. In other words, you can send or receive money instantly at any time.

Exception for Non-Eurozone PSPs:

PSPs located outside the Eurozone can get temporary permission from their national regulators.

They don’t have to offer instant credit transfers in euros beyond a certain limit per transaction from non-euro-denominated accounts.

This limit (set by the regulator) cannot be lower than EUR 25,000.

The permission lasts for a year but can be extended based on the regulator’s assessment.

Fair Charges:

PSPs cannot charge more for instant credit transfers than they do for other similar credit transfers.

Additional Requirements:

The IPR includes specific rules that differ from the existing Payment Services Directive (PSD2).

These rules cover areas like payment order receipts, value dates, availability of funds, and liability.

The SEPA Regulation also adds extra requirements for instant credit transfers.

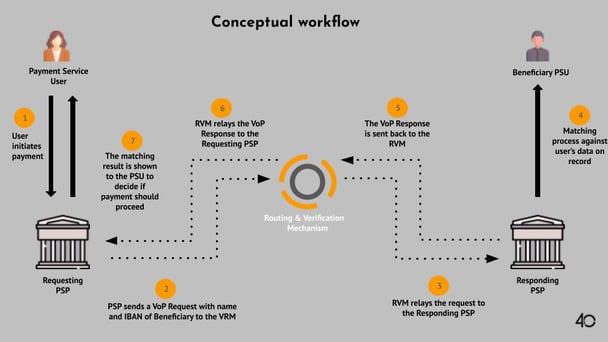

What is VoP?

VoP stands for Verification of Payee.

It’s a service required by the Instant Payment Regulation (IPR) for all credit transfers (both instant and non-instant).

What Does VoP Do?

When you want to send money (a credit transfer), your Payment Service Provider (PSP) must verify the payee (the person or entity receiving the funds).

VoP matches the IBAN (International Bank Account Number) with the payee’s name.

The payee’s name can be either:

The full name (for individuals).

The commercial or legal name (for businesses or organizations).

How Does VoP Work?

VoP provides different levels of matches:

No match: The name doesn’t match the IBAN.

Almost match: There’s a partial match.

Other possible match levels.

The payer (you) receives this information and decides whether to authorize the payment.

Important Point: Your PSP must offer VoP, regardless of how you initiate the payment (online, mobile app, etc.).

The IPR strives to make payments faster and more convenient for EU members. VoP ensures that your money goes to the correct recipient by verifying their name against the account details. Additionally, 40 Consulting can guide and assist you through this process.