From Barter to Blockchain: Tracing the Evolution of Payments Through Time

PAYMENTS

4/4/20245 min read

Throughout history, the exchange of goods and services has been the foundation of economic activity. Over time, payment methods have undergone significant changes, reflecting shifts in society, technology, and the global economy. This article takes you through the ages, from the earliest barter systems to the latest cryptocurrency advancements. Each stage in the evolution of payment methods represents humanity's pursuit of efficiency, security, and convenience. Come with us as we explore the intriguing history of payments and the innovations that have revolutionized our trade today.

Barter System

Before the invention of money, people relied on a barter system where goods and services were exchanged directly between individuals. For instance, a farmer might trade some of his crop for a potter's clay vessels. This system worked well in small communities where people's needs were similar. However, it had some limitations. The "double coincidence of wants" problem meant that both parties needed something the other desired, making complex trades difficult. Additionally, there was no standard measure of value, which made larger or more diverse transactions more complicated.

Bartering was an early trade method that helped develop more advanced economic systems despite its challenges. However, a more flexible and standardized payment method was needed as societies grew and trade networks expanded. This need led to the development of commodity money, which marked a significant leap in the history of payments.

The transition from bartering to commodity money was driven by the need to solve barter's inherent limitations and accommodate the complexities of expanding trade networks. Several key factors precipitated this change:

- The bartering system required a double coincidence of wants, which became increasingly challenging in complex economies.

- Commodity money was more divisible, portable, durable, and standardized than bartered goods.

- Precious metals became a universally recognized medium of exchange that facilitated trade over longer distances.

- Commodity money supported the expansion of trade, specialization, and the development of markets in larger, more complex societies.

These factors, combined with innovations in metalworking and establishing governance structures capable of standardizing and enforcing the use of commodity money, led to the widespread adoption of this new economic system.

Commodity Money

As societies progressed, trade became more complex, which led to the development of standardized forms of currency. This gave rise to commodity money, which refers to intrinsic value items. Historically, livestock was among the first commodities used as currency, followed by grains, shells, and later precious metals such as gold and silver. For example, salt was so valuable that it was used as currency in ancient Rome, highlighting its worth in preserving food.

The shift towards commodity money was the initial step towards a more widespread trade system, allowing for transactions to occur over long distances and between larger groups of people. However, certain physical properties of commodities, like perishability and varying quality, soon showed that a more consistent and long-lasting currency was necessary.

Coinage

The creation of coinage in Lydia (modern-day Turkey) around 600 BCE significantly changed payments. These coins were the first of their kind, made from electrum, a natural alloy of gold and silver. They were stamped with official marks to show their authenticity and value. This innovation revolutionized trade by allowing more precise valuations and expanding trade networks.

The use of coins as a form of currency spread across various civilizations, such as Greece and Rome, and eventually the rest of the world. This spread highlighted the effectiveness of coins as a medium of exchange, unit of account, and store of value. One of the significant advantages of using coins was that it allowed people to accumulate wealth and led to the development of complex economic systems, including taxation and state-sponsored economies.

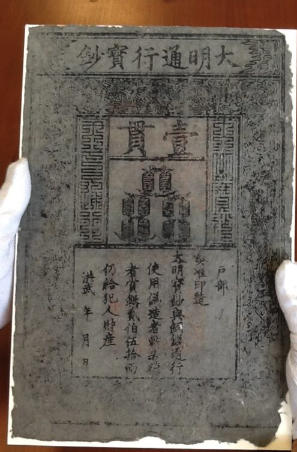

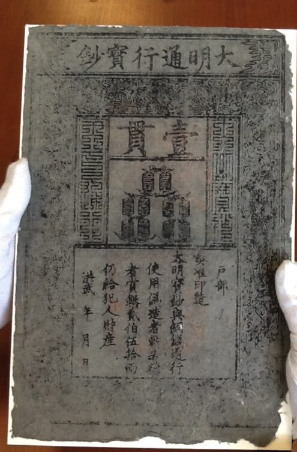

Paper Money

During the Tang dynasty (618–907 CE) in China, the introduction of paper money marked a significant evolution in payments. Its formal issuance occurred around the 11th century. This was a revolutionary concept that represented a shift from intrinsic value to symbolic value. Paper money was lighter, easier to transport, and could be produced in larger quantities than coins.

The use of paper money gradually spread worldwide, with European nations adopting it during the 17th century. This shift was mainly driven by the necessity to finance growing trade and military expenses, demonstrating paper money's versatility and flexibility.

Electronic Payments

In the late 19th century, electronic payments became a new trend with the introduction of wire transfers. This gained momentum with the arrival of the internet, leading to the evolution of electronic payments. Credit cards were launched in the mid-20th century and quickly became a popular consumer finance tool. They allowed people to make secure transactions without using physical currency, offering convenience to the users.

During the late 20th and early 21st centuries, online payment platforms such as PayPal became increasingly popular. These platforms helped to democratize electronic payments, making them available to individuals and small businesses worldwide. This era can be defined by digitalizing financial transactions, offering unprecedented convenience and speed.

Cryptocurrencies

The emergence of Bitcoin in 2008 marked the beginning of cryptocurrencies, which operate on blockchain technology. This framework offers a secure, transparent, and decentralized platform for transactions.

Cryptocurrencies are gaining popularity due to their ability to ostensibly offer privacy, reduce transaction fees, and remove the need for central authorities such as banks. Although they face challenges in regulation and adoption, cryptocurrencies represent a significant move towards digital and decentralized financial systems.

Conclusion

The history of payments demonstrates human innovation and the pursuit of more efficient, secure, and inclusive financial systems. From barter to cryptocurrencies, each advancement has been driven by the needs of its time, shaping economies and societies in significant ways. Looking towards the future, it's evident that the journey of payment systems is far from over, as technology has the potential to revolutionize further how we transact and interact economically.

This journey through time gives us a better understanding of our economic past and offers insight into global finance's future. The question now is, what will be the next significant milestone in the evolution of payments?